Datanami

Datanami EnterpriseAI

EnterpriseAI HPCwire Japan

HPCwire Japan QCwire

QCwire HPC & AI Wall Street

HPC & AI Wall Street

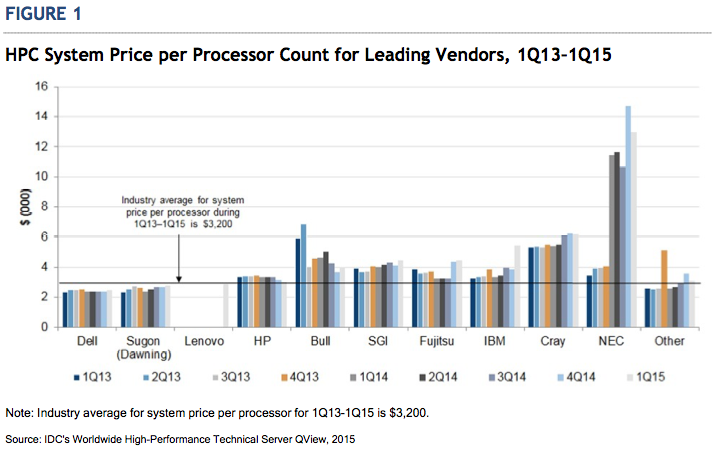

IDC reported the worldwide technical server market grew more than 10 percent on a year-over-year basis to more than $2.5B for Q1 2015 versus Q1 2014. There was good news for Lenovo, which bumped up to third place behind HP and Dell, while IBM fell from second to a distant fourth. Not surprisingly, the ripples from the sale of IBM’s x86 business are still jostling server market waters.

Bob Sorensen, Research Vice President in IDC’s High Performance Computing group told HPCwire, “IDC expects x86-based will continue to capture over 80% of HPC server revenue, but key wins for the OpenPOWER Foundation could build on the momentum of IBM Power’s success in the recent DOE CORAL acquisitions and make a dent in Intel’s x86 market dominance over time.”

These were among findings presented in IDC’s just released Worldwide High-Performance Technical Server QView Report. Lenovo is doing a better-than expected job retaining former IBM x86 customers as well as growing strongly on its own in the U.S. enterprise computing market and in China, according to IDC. For IBM, the hit was not unexpected, and as IDC noted the IBM Power Systems business has growing momentum.

One challenge facing system- and chipmakers is the need to bridge performance requirements of technical computing and big data.

“The HPC sector is currently looking to serve two somewhat distinct masters; the traditional compute-centric modeling and simulation space where high flops counts are king, and the rapidly growing HPDA (high performance data) space where considerations of efficient and effective data movement – not computational capability – is the critical performance metric,” said Sorensen.

“Any chip vendor – or consortium of vendors – that wants to succeed going forward will face the daunting task of addressing the somewhat distinct performance requirements of both spaces,” he emphasized.

IDC believes there will likely never be a one-size fits all HPDA architecture and that HPDA architects will increasingly need to design with an eye towards HPDA system flexibility. “They will need to draw on and design within a fully supported and tightly integrated ecosystem where single use-case HPDA systems can be readily assembled out of existing COTS (commercial off the shelf) or related HPC subcomponents for a specific workload or application. A processor base that best supports that philosophy stands a strong chance of success in the market.”

Sorensen also noted a nascent trend by suppliers looking to differentiate their products by offering ARM-based options: “Gains will be small at first, and future viability will depend heavily on the development of a heretofore limited HPC software ecosystem for ARM chips. We’re also closely watching the spate of indigenous processors developments, coming out of Japan and — more notably and aggressively — China, looking to build processors targeted initially for domestic HPC inclusion, but with a long-term prospect to sell those chips in foreign markets. Progress here will come slowly and not without significant fits and starts,” said Sorensen.

Sorensen also noted a nascent trend by suppliers looking to differentiate their products by offering ARM-based options: “Gains will be small at first, and future viability will depend heavily on the development of a heretofore limited HPC software ecosystem for ARM chips. We’re also closely watching the spate of indigenous processors developments, coming out of Japan and — more notably and aggressively — China, looking to build processors targeted initially for domestic HPC inclusion, but with a long-term prospect to sell those chips in foreign markets. Progress here will come slowly and not without significant fits and starts,” said Sorensen.

The rise of Chinese server and chip makers is also a growing theme according to the IDC QView Report. Here’s a brief excerpt:

“In the Chinese market, Chinese technical server vendors appear to be making a move against their competitors from the United States and Japan. In addition to Lenovo’s explosive growth — essentially a strong reflection on the ability of the firm to retain IBM x86 customers — another Chinese technical server supplier, Sugon, saw its first-quarter 2015 year- over-year revenue increase by over 60%.

“Although Sugon is only about one-seventh the size of Lenovo — and is currently making sales primarily in the Chinese market — its overall growth rate is outpacing most competitors. Lenovo has said publicly that it expects to lose some IBM x86 server business worldwide but make up for this with increased business in China. But Lenovo is pushing hard into the European high-performance computing (HPC) market by joining the European Technology Platform for HPC (ETP4HPC) and establishing a European HPC innovation center in Stuttgart, Germany.”

Sorensen further noted, “Chinese telecommunications giant, Huawei, which makes 75 per cent of its revenue overseas through the sales of telecomm equipment and smart phones, is also well positioned to expand sales of its servers globally. In addition these and other Chinese server vendors will benefit from recent activities by some of the larger Chinese data center and cloud service providers looking to expand their presence overseas.”

One example: “A few months ago, China’s Alibaba‘s – the world’s most popular destination for online shopping with transactions totaling more than those of eBay and Amazon.com combined – announced it was preparing to open its first overseas cloud data center in Silicon Valley as part of a larger global push. Chinese server vendors could be major supplier of hardware technology to fuel this and other Chinese data center expansions globally,” said Sorensen.

Looking ahead generally IDC also predicted continued growth of smaller, more differentiated technical server suppliers — like NEC, Cray, SGI, Fujitsu, Hitachi, T-Platforms, and Atos-Bull — to develop and compete effectively with relatively higher-cost and higher-performance systems using more proprietary and custom technology. IDC also noted white-box suppliers had a 26% first-quarter 2015 rise rate and appear to be targeting the major brand-name technical server vendors with more than just lower prices

IDC will present its latest full HPC market update at its annual ISC breakfast next week in Frankfurt, Germany. More information about the Worldwide High-Performance Technical Server QView Insight Report can be found at: https://www.idc.com/getdoc.jsp?containerId=IDC_P225