Datanami

Datanami EnterpriseAI

EnterpriseAI HPCwire Japan

HPCwire Japan QCwire

QCwire HPC & AI Wall Street

HPC & AI Wall Street

There was much to unpack in Intersect360 Research’s pre-SC20 Market Update presented by Addison Snell, cofounder and CEO, in a webinar yesterday. The COVID-19 pandemic, of course, continues to roil the forecast waters. But long-predicted HPC cloud demand has actually materialized and is booming. New user study preference data spotlighted strengthening AMD CPU and GPU prospects. Big systems sales (e.g. exascale and the like) drove strong HPC spending in 2019 and have continued in 2020 with COVID-related spending pitching in but overall 2020 HPC sales will decline anyway.

While there was some review material, Snell added fresh data and did a nice job of connecting the dots outlining the current HPC market landscape. The slides (~ 60) and recorded video (90 minutes) are freely available and the slides make for fast reading.

Here are a few highlights from the presentation:

- Intersect360’s 2020 HPC market forecast, revised downward 10.1 percent from the original forecast in March, now calls for a 3.7 percent year-over-year decline and seems to be holding true. U.S. will be the hardest hit region, down 6.8 percent, according to Intersect360. Questions remain for 2021, primarily around whether COVID-19 will linger in which case any market rebound will have to wait.

- Cloud computing demand is booming despite (and perhaps a little bit because of) the pandemic. Moreover, directly measured cloud revenues (up 17.8 percent last year) likely understate cloud’s true growth because so much cloud revenue ends up buried in other reported spending categories, (e.g. software, SaaS, etc.).

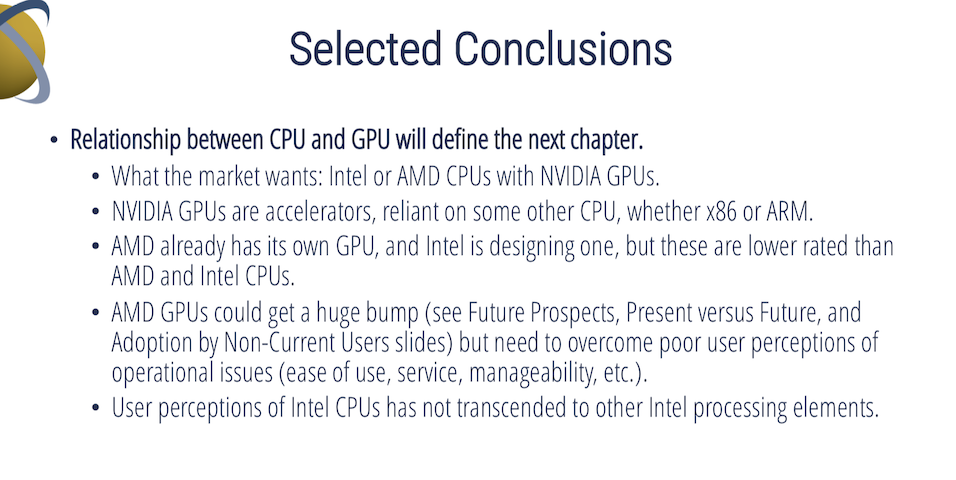

- Intersect360’s latest user study suggests, among many other things, that AMD’s CPUs and GPUs have excellent prospects even as the chip industry consolidation continues. IBM’s Power processor line, not so much. Intel is still the big dog but maybe slipping.

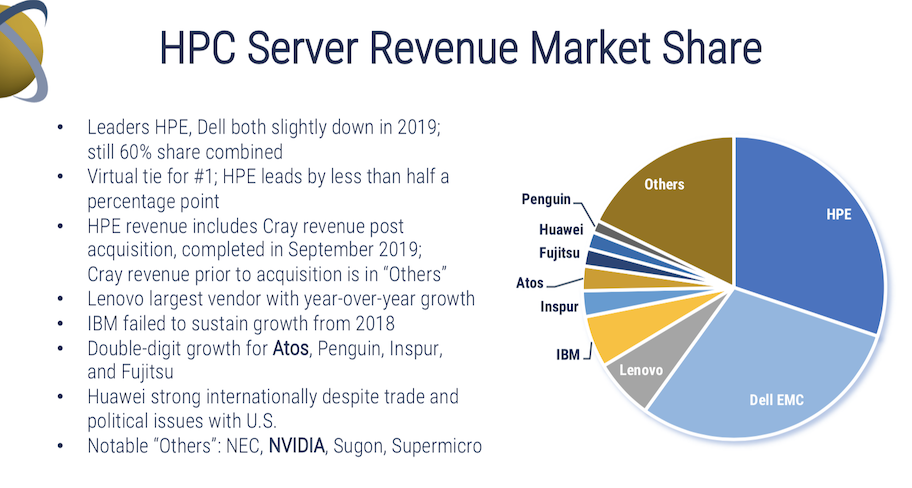

- Server giants – HPE and Dell EMC – were slightly down from 2018 but still lead the pack. IBM was also down. Conversely, Atos, Lenovo, Penguin, Inspur, and Fujitsu were the big growers (double digits in 2019).

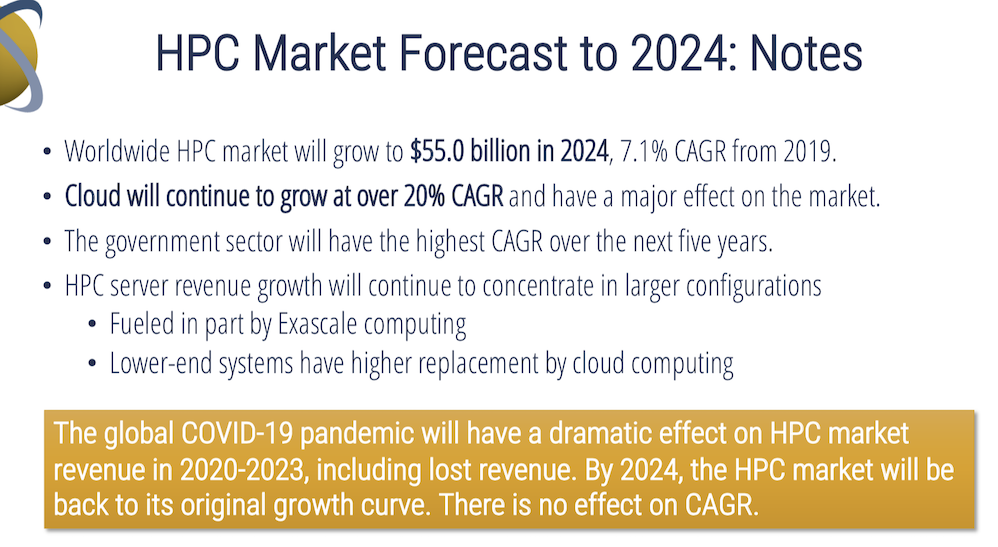

- Closing the books on 2019 (completed in September), Intesect360 reports the overall HPC market was $39 billion, up 8.2 percent. If the latest 2020 forecast stays true, that will fall to around $37.5 billion this year. If 2021 rebounds (pandemic cautions apply here) the total HPC market could still hit $55 billion in 2024 representing a 7.1 percent CAGR.

“Back in March, the assumption was that Asia Pacific would be the hardest hit followed by EMEA, and then followed by followed by North America, US, and Canada, by the time we actually published the forecast, it reversed and we were looking at a bigger effect in US and Canada,” said Snell. “We’re going to have to monitor how these regions look as we get into adjusting our forecast next year. Early indicators are that 2020 is trending according to how we forecast.”

The assumption had been the pandemic would diminish substantially in 2021 and the buying slowdown – largely stemming from deferred purchases – would end and catch-up spending would ensue. “Now I think that’s going to be in doubt,” said Snell. “The longer it (pandemic) lasts, the more we will find spending is not only delayed but cancelled.”

One persistent demand driver despite the pandemic is AI; its rapid adoption in HPC and throughout the enterprise remains robust in the face of a more generalized anemic mid-to-lower tier server market. Snell contrasted the AI experience with what happened when ‘big data’ was the buzz phrase of the day.

Snell said, “Think about what the supercomputing tradeshow looked like in 2013 and 2014. It was a big data show, and everyone was all up on big data. We [Intersect360] were saying that big data [and] data science is real, but it’s not having an effect on HPC budgets and not having an effect on the enterprise budget as a whole. And that was true. [Many companies invested] in big data appliances, big data business units, almost all of which failed.”

Machine learning is different not least because of its close connection to enabling hardware architecture and accelerators. What’s more, ML technology is increasingly used in both AI and mixed HPC/AI workloads. “In this case GPU-heavy configurations can serve both masters in HPC and machine learning well. That is a relevant trend,” he said. ML is also an important driver of increased cloud spending by providing users with flexible access to the rapidly-changing AI technology (accelerators, software tools, et al.) without necessitating major infrastructure commitments.

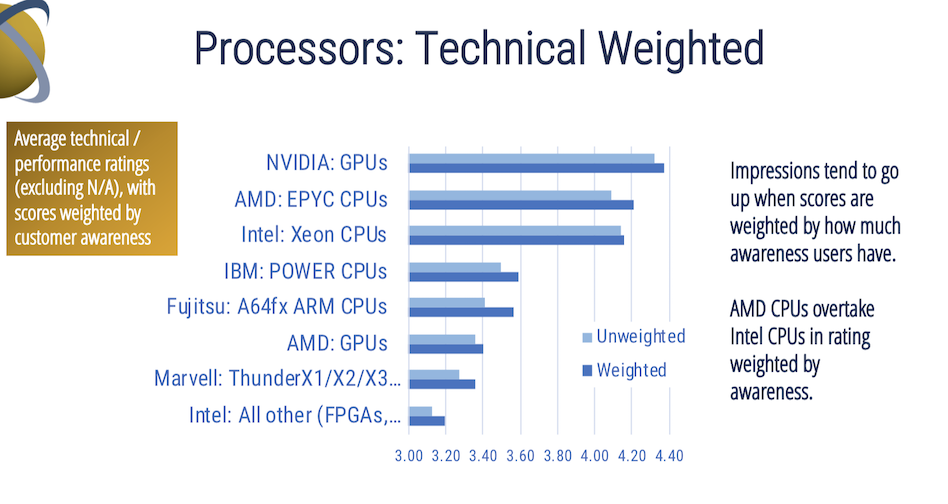

Intersect360 also presented results from the processor portion of its User Vendor Rating study which covered processors, storage, servers, and major cloud providers.

Snell said little about the other categories but did note, “AWS almost swept the categories. Projected market share gain was best for Azure. But the real thing I’m saying [for] cloud is there was a clear top three on almost every question, which is AWS, Azure and GCP (Google) were closely grouped at the top on every question. Then there was a big drop to number four. Then there’s a big drop down from number four to everything else. Maybe sometime next year, we’ll give a more full public presentation on all of that.”

Digging into the processor results, Snell noted the ongoing consolidation in the market. He said while user preference is to be able to pair Nvidia GPUs with whichever processor they wish, vendor strategies are to pair their branded offerings. AMD has started doing this (AMD CPU and GPU) and has had notable wins in the exascale program. Intel’s planned Aurora system also pairs Intel CPUs and GPUs.

Snell said, “CPU and accelerator consolidation is going to be a major trend for next year and we’re going to be talking about it both in terms of a literal consolidation – Nvidia acquiring Arm, AMD acquiring Xilinx, Marvell acquiring Inphi but canceling ThunderX3 – and technology consolidation.

“Technology consolidation is, I think, even more important. What we’re going to start seeing is all Intel environments with Xeon CPUs and Xe GPUs on an Intel fabric or AMD Epyc CPUs and Instinct GPUs, and Nvidia Arm CPUs with A100 or future Nvidia GPUs. That is the trend for 2021.”

Along similar lines, Snell thought big server companies that didn’t have their own fabric might be at a disadvantage moving forward at least when selling into the high-end. HPE/Cray has Slingshot. Fujitsu has Tofu. Atos has a fabric. It is interesting to note that Intel, whose Omni-Path fabric had decidedly mixed market traction, spun out Omni-Path in September as Cornelis Networks. That will bear watching. Nvidia, of course, acquired Mellanox (and its InfiniBand portfolio). Dell EMC and Lenovo are two high-end server makers without their own fabrics. We’ll see.

Snell also spent quite a bit of time discussing the challenge in measuring HPC ROI. This portion of his presentation covered the same ground he presented in a recent HPCwire commentary (ROI: Is HPC Worth It? What Can We Actually Measure?). Intersect360 will again be on the virtual SC20 agenda with Snell moderating a SC panel on storage. It will tackle, among other things, approaches and trends in tiering storage. (Track 8, Panel 116, Nov. 17, 1:30 ET, The Diverse Approaches to Tiering HPC Storage).