Datanami

Datanami EnterpriseAI

EnterpriseAI HPCwire Japan

HPCwire Japan QCwire

QCwire HPC & AI Wall Street

HPC & AI Wall Street

Hyperion Research delivered its annual HPC market update at SC21 today. Much of it echoed Hyperion’s earlier mid-year report: the 2020 HPC market (on-premise) finished around $28B slightly up (~1.1 percent), roughly what was forecast in June. The gain was mostly due to the early standing-up of Fugaku. Yesterday’s surprise was that 2021 looks stronger than expected, driven by acceleration of cloud HPC, rapid GPU adoption, big systems sales and all things AI. The caveats, noted Hyperion, are pandemic and supply chain uncertainties.

“In 2020, the market surprised us,” said Earl Joseph, Hyperion CEO. “It was actually up by a little more than one percent, just shy of $14 billion for the servers, and roughly $28 billion if you count all the other parts of the market. The reason the market was up was because Fugaku (Japan’s supercomputer) came in at roughly a billion dollars. If you take Fugaku out, the market was actually down seven to eight percent because of COVID [and] the supply chain issues related to COVID.”

Hyperion initially expected rough sledding for 2021 but has been pleasantly surprised. “Looking [at] the first half of 2021, it looks very strong. We’re seeing some very strong successes with a number of the vendors. We are still concerned with the second half of the year, whether the supply chain issues and some of the other economic issues with COVID may have an impact, but at the moment, the first half the year looks really strong,” Joseph said.

Coalescing Hyperion’s hour-plus, eight-section, six-speaker HPC market update into a brief article is too ambitious. Fortunately, Hyperion has posted the slide deck and videos of the presentations on its website. Joseph noted that given the pandemic-related constraints on face-to-face activities generally, Hyperion planned to post more material on its site for public consumption than in the past.

Presented here are just a few highlights from the presentations, which included HPC market; AI and HPDA; exascale; edge computing; HPC applications; HPC in the cloud; storage and interconnect; and quantum computing.

Let’s start with Hyperion’s conclusions.

The trends cited — maybe excepting 2021’s strength — are familiar. One change from the past in Hyperion’s latest report is the use of new subdivisions for supercomputing, introduced earlier this year – Leadership/Exascale-class systems; Supercomputers-Large ($3M and up); and Supercomputers-Entry Level ($500k to $3M). Note that the lower boundary for the overall supercomputing division ($500k) has not changed.

The changes seem to make sense. Sales of very large systems can easily skew the category, making it look healthier than warranted and perhaps less relevant to mainstream large system buyers.

“These are the truly large machines, the leadership classes we’re referring to here, [which] are generally purchased by large governments around the world,” said Joseph, who noted the current buying binge for leadership and exascale systems would eventually cool. (Supercomputing sales have long been subject to boom-bust cycles.)

Hyperion is forecasting a 7.9 percent overall five-year growth for HPC segments, but with a flat-to-down slightly fifth year (chart below) for all segments (server, storage, middleware, applications and service). Still, HPC on-prem revenues would hit $40B in 2024 — a major milestone — and fall back to $39B in 2025.

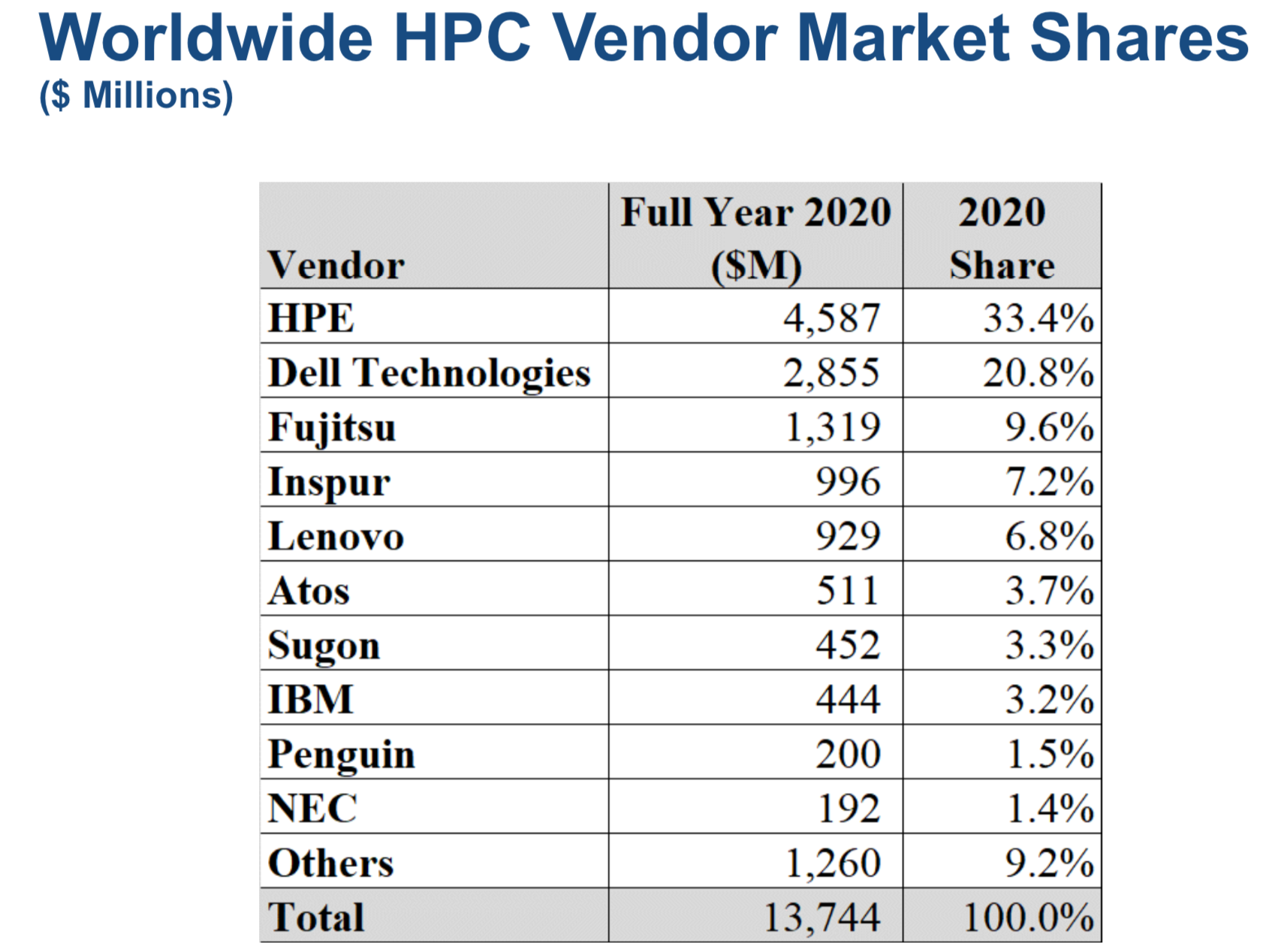

Joseph pointed out there have been market share changes among HPC server vendors recently. “HPE, with its acquisition of Cray and SGI, is a clear market leader with roughly a third of the market,” said Joseph. “Dell is doing very well [at] around 21 percent and is growing fairly quickly. You can see quite a mix of vendors here [see slide below]. And because of Fugaku, Fujitsu is now number three in the market at 9.6 percent. We’re seeing a lot of changes in the market, and you’ll see that when one vendor sells a very large system, you can see them move up the list quickly.”

Joseph shared a few results from a recent end-user study. Hyperion, he said, surveys end users roughly every year to 18 months. “We survey at least 1000 systems – it’s usually 1200 to 1400 across maybe 140 different sites because the average site has seven to eight systems in it,” he said.

“First of all, and no surprise because of COVID the economic issues, the [average] length of time somebody keeps an HPC system is growing. It is now at 4.2 years. Previously, it was running closer to 3.8 years. So, we’re seeing a fair amount of delay in upgrades,” continued Joseph. He suggested several potential reasons, ranging from users simply holding onto budgets or taking longer because the buying process takes longer under COVID restrictions. “In the more virtual world, it’s harder to do contracts and move them through an internal system,” he said.

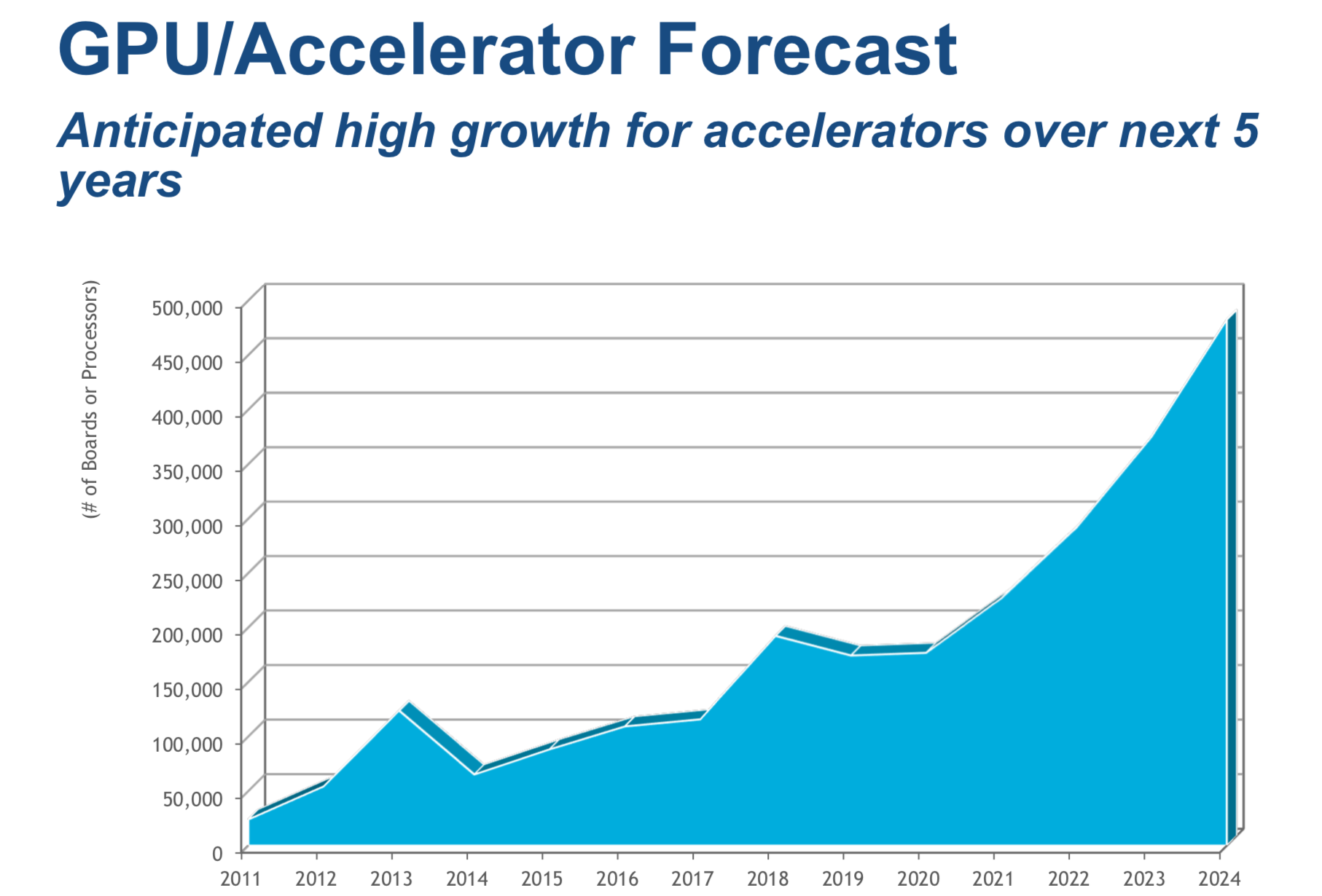

One interesting nugget from the survey was the growth in accelerator use. “We had a lot of surprises in this study. One of the larger ones [is] that around 83 percent of the sites have some acceleration in their system,” said Joseph. While many sites still haven’t fully moved to accelerators, he said, “The number of sites that actually have accelerators – either using them for mainstream AI processing, traditional modeling simulation, or just doing experiments – is the majority of the market. So, we’re seeing just tremendous adoption there.”

“In this , we’re showing the different types of AI, machine learning, deep learning approaches that are being used,” said Joseph. “And as we’ve been saying, machine learning is the number one application. Deep learning is increasing, but deep learning has had some setbacks as far as transparency [and being] explainable. We think longer-term deep learning is going to be extremely strong. We think machine learning is more the bulk of the market. But you’ll see here in this chart, there’s a number of other technologies that are used in different places. Graph analytics, of course, is one of the stronger ones. But we expect to see a lot of new and different types of AI technology.”

Hyperion’s market update was extensive and is best tackled by directly reading the slide deck and watching or listening to relevant presentations. The list of sections and analyst names is below. Follow this link to learn more.

Hyperion SC21 Update

- HPC Market Update, Earl Joseph

- Highlights of AI and HPDA growth in HPC, Alex Norton

- A Quick Update on Exascale Systems, Bob Sorensen

- Edge Computing and HPC, Steve Conway

- HPC Applications Update, Melissa Riddle

- New Trends on Using Cloud for HPC Workloads, Alex Norton

- Perspectives on Storage and Interconnects, Mark Nossokoff

- Quantum Computing: Moving Out of the Lab? Bob Sorensen

Slides: Hyperion Research